Australia's Home Battery Revolution: How Distributed Energy Storage is Reshaping the National Electricity Market, Commodity Supply Chains and Energy Transition

Twelve months ago, battery storage was still a comparatively niche layer of Australia's energy system. In the year since, it has become the technology policymakers, market operators and investors talk about first. The federal Cheaper Home Batteries rebate, launched 1 July 2025, has turned household storage into a mass-market product, while grid-scale batteries have overtaken hydro as the most frequent price-setter in the National Electricity Market (NEM). At the same time, coal generators are becoming less reliable just as renewable output keeps setting records, and the commodities that make batteries possible - lithium, nickel, cobalt, and graphite - are moving through one of their most volatile pricing cycles in years. This report brings together the policy, economic, generation, commodity, and risk threads of that story.

COMMODITIESMOST RECENT

Dewashish Ranade

7/7/20268 min read

POLICY: POWERING ADOPTION FROM THE TOP DOWN

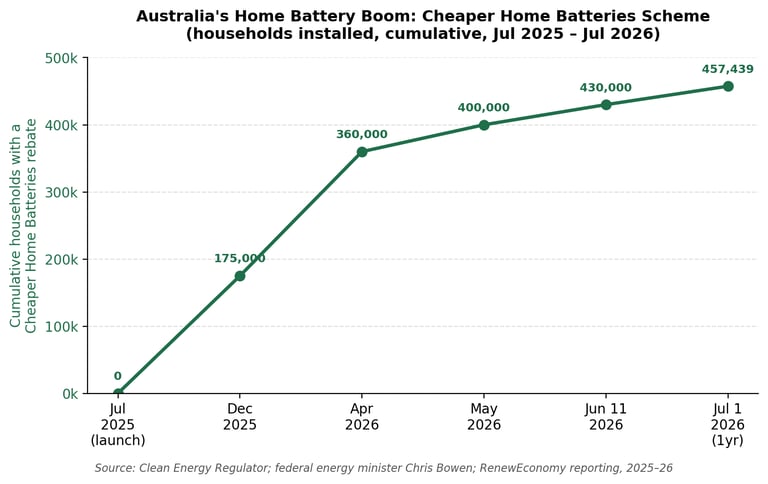

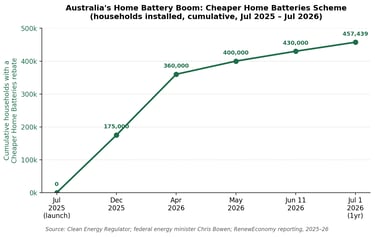

The single biggest driver of Australia's distributed battery boom has been the federal Cheaper Home Batteries programme. Since its July 2025 launch, the scheme has subsidised roughly 30% of the upfront cost of a home battery, and uptake has defied expectations. By its first birthday on 1 July 2026, Energy Minister Chris Bowen confirmed 457,439 households had installed a battery under the rebate - roughly one in every 17 Australian homes - adding well over 13GWh of behind-the-meter storage.

That success created its own problem: the projected four-year cost blew out toward $14 billion before Canberra rewrote the rules in December 2025, tapering the subsidy above 14kWh and again above 28kWh to slow the rush toward oversized systems. The changes, effective 1 May 2026, cooled the market - installed capacity fell from April's record 2.4 gigawatt-hours to 1.5 GWh in May - while average system size settled from the 40-50kWh boom-era range toward 20-30kWh. On 1 July 2026 the government added a second policy, the Solar Sharer Offer, giving households three hours of free daytime power designed to work alongside batteries, pulling midday solar into the evening peak.

State governments have layered their own schemes on top - NSW's Peak Demand Reduction Scheme, a reinstated Victorian rebate covering apartments and small businesses, and various community battery programmes. AEMO's Draft 2026 Integrated System Plan formalises the direction: 55GW of dispatchable storage is now built into the least-cost pathway to 2050, alongside two-thirds of the remaining coal fleet closing by 2035.

WHAT BATTERY STORAGE MEANS FOR THE ECONOMY

Battery storage is now a genuine line item in Australia's economic story, not just its energy one. Between 2017 and December 2025, large-scale storage projects reaching financial close totalled A$31.4 billion across 20.6GW of capacity, and 2025 alone saw 2GW/5.1GWh commissioned - a 233% year-on-year jump that made Australia the world's third-largest utility-scale battery market behind only the United States and China. Combined with renewable generation investment, 2024's $12.7 billion in clean-energy financial commitments was, at the time, the largest single year of clean-energy investment in the country's history.

The flow-through benefits are measurable. AEMO estimates passive, uncontrolled home batteries shaved close to 600 MW off the evening peak nationally in early 2026, simply through consumers using their own stored solar. The Climate Council calculates grid-scale batteries had displaced 30 petajoules of gas-fired generation by the end of February 2026, insulating households from gas-price volatility tied to global conflicts. Storage is also a regional jobs story: individual big-battery projects each support 100-200 construction jobs, and the sector's growth is drawing international capital seeking a politically stable, high-growth market.

AUSTRALIA'S POWER GENERATION SNAPSHOT: JUNE 2025 - JUNE 2026

Over the past financial year, the NEM supplied roughly 200 TWh of electricity worth more than $25 billion, from a fleet whose registered capacity mix still reflects the transition underway: rooftop solar around a quarter, black coal about 16%, wind near 14%, gas about 13%, grid-scale solar around 12% and hydro roughly 8%, with brown coal shrinking toward 5% as grid-scale batteries become a fast-growing slice of new capacity.

Quarter by quarter, the trend has been consistent. Renewable generation set a new March-quarter record of 46.5% of NEM supply in 2026, up from 43.0% a year earlier, while coal-fired output fell to a new Q1 low and gas generation dropped to its lowest level since 1999. The December 2025 quarter was the standout: for the first time, renewables and storage supplied more than half of the NEM's energy needs for a full quarter - a result AEMO called a landmark moment. Underlying demand kept climbing regardless, up 1.2% YoY in Q1 2026 to a record 25,496MW, driven by electrification, population growth and the first large-scale data-centre connections, though record rooftop solar output offset much of that growth at the grid level.

PEAK DEMAND, PEAK GENERATION, AND THE PRICE STORY

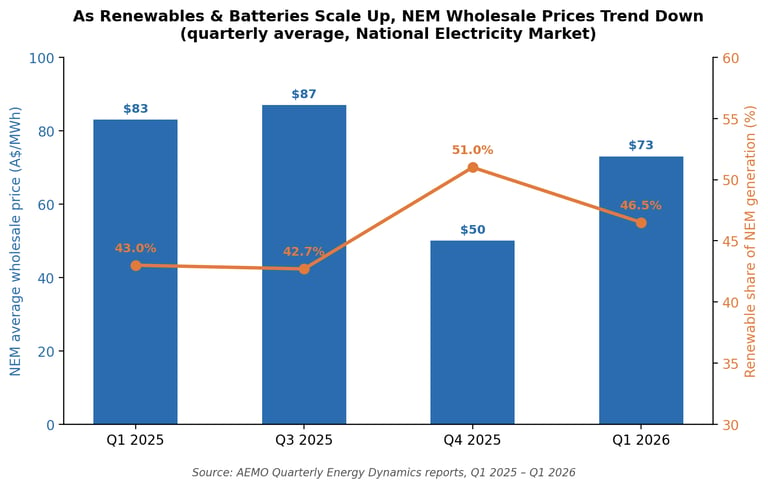

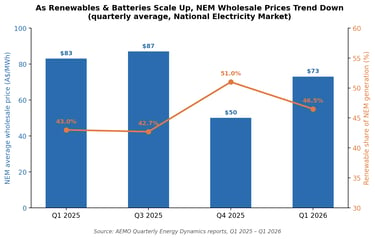

The clearest signal of the storage build-out shows up in wholesale prices. NEM-wide average wholesale prices fell from $83/MWh in Q1 2025 to $50/MWh in Q4 2025 - a 44% YoY fall - before firming to $73/MWh in Q1 2026 as summer heat lifted demand.

Batteries are increasingly the mechanism behind that fall. In Q1 2026, combined battery charge and discharge activity set prices in around 32% of trading intervals across the NEM - more often than hydro, and over 40% in NSW and Queensland - displacing the coal, gas and hydro generators that used to dictate peak pricing. That is visibly flattening the old evening spike: daytime prices have lifted slightly as batteries charge on cheap midday solar, while evening peak prices and volatility have fallen as batteries discharge into the peak instead of gas. The relationship isn't perfectly one-directional - South Australian prices jumped 33% in Q1 2026, but AEMO attributed almost the entire rise to a single extreme weather day, not a structural reversal. Peak demand and peak generation are also drifting apart: rooftop solar and batteries are cutting operational grid demand even as underlying total demand hits records, meaning less of the fleet is needed to meet an increasingly concentrated evening peak.

RENEWABLES EXPANSION: SOLAR, WIND, AND HYDRO'S SYMBIOSIS WITH STORAGE

Batteries and renewables are increasingly two halves of one story. Grid-scale solar output rose 13% YoY in Q1 2026, and wind generation grew across most of the past year, but it is storage that has turned intermittent output into dispatchable capacity-cheap batteries do not just complement solar; they unlock its full potential. Planning a shift? - Now assuming more solar and batteries, and less wind and gas capacity, than earlier versions.

Hydro's role is smaller but strategically important as a flexible, dispatchable backup - Snowy Hydro alone controls more than 5,000MW of flexible capacity, and its delayed Snowy 2.0 pumped-hydro project remains a bellwether for how much long-duration storage the market can add beyond batteries. The risk of leaning too heavily on short-duration lithium-ion storage was illustrated starkly in late June 2026, when South Australia swung from three days above 100% renewable supply to its worst wind drought in seven years within ten days - its fleet of four-hour batteries emptied and gas had to fill the gap, underlining argument for a diversified mix of solar, wind, batteries and longer-duration storage such as pumped hydro.

COAL-FIRED GENERATION: RETREAT, RELIABILITY AND RISK

Coal remains a large share of Australia's fleet, but its trajectory is unambiguous. AEMO's Draft 2026 Integrated System Plan expects two-thirds of the remaining coal fleet to close by 2035, with all units retired by 2049; several closures - Eraring, Bayswater, Vales Point, Yallourn and Callide B among them - have already been brought forward. EnergyAustralia's Yallourn plant, Victoria's oldest coal station, is now scheduled to close in mid-2028, four years earlier than planned, partly replaced on-site by a 350MW battery.

The immediate risk is reliability, not longevity. In the 2025-26 summer alone, there were 90 unscheduled coal outages, leaving around a quarter of coal capacity offline on average at any given time, per the Clean Energy Council. That ageing fleet is precisely the gap grid-scale batteries and gas peakers are being built to cover - but the Council also flags just 2.3GW of new renewable generation reached financial close in 2025, one of the lowest totals in a decade, raising real questions about whether replacement capacity is being built fast enough to match coal's exit. Coal generators can still set high marginal prices when they run, but do so less often as batteries and renewables take over price-setting each quarter

BATTERY COMMODITIES: LITHIUM, COBALT, NICKEL, AND GRAPHITE

Australia's status as the world's largest lithium producer and a top-five cobalt and rare-earths exporter puts it on both sides of the battery boom - supplying the metals as well as installing the batteries. The June 2026 Resources and Energy Quarterly projects lithium export earnings rising from $9.9 billion in 2025-26 to a peak of $12.5 billion in 2026-27, before moderating toward $10 billion by 2030-31 as global supply catches demand; mine output is expected to grow roughly 8% a year to 2031 on expansions at Greenbushes, Pilgangoora and Kathleen Valley. Nickel earnings, battered by weak prices through 2024-25, are forecast to recover to around $1.7 billion by 2030-31, while other critical minerals (manganese, rare earths, antimony and cobalt-linked streams) grow from $5.5 billion to $7 billion over the same period.

Prices tell the volatility story behind those figures. Lithium carbonate prices in China nearly doubled between December 2025 and January 2026 on supply disruptions and a looming battery-export tax change, before retreating through the June quarter as previously suspended mines - including Australia's own Bald Hill and Finniss projects - prepared to restart. Nickel jumped roughly 30% MoM in December-January after Indonesia slashed its 2026 mining quota, a shock expected to help lift prices back toward US$17,000/t by late 2027. Cobalt has been driven by a different lever: the Democratic Republic of Congo, source of over 70% of global supply, has capped 2026-27 exports at roughly 96.6 kT - around half its 2024 peak - turning a structural surplus into a feedstock deficit.

The bigger overhang across all four commodities is processing, not mining: China controls more than 80% of midstream and downstream battery-material processing globally, including a near-monopoly of over 95% in precursor cathode and LFP cathode materials, meaning Australian ore typically still needs Chinese refining before it becomes battery-grade material.

RISKS AND VULNERABILITIES OF THE STORAGE BUILD-OUT

The scale-up of home and grid batteries carries risks beyond commodity supply chains. Fire safety remains the most visible public concern, even though Australian standards require batteries to withstand crushing, nail penetration, overcharging and short-circuit testing before approval, and industry data suggests certified lithium and LFP home batteries carry a low absolute thermal runaway risk. Insurers remain more cautious about utility-scale systems, still pricing in fire risk based on isolated but high-profile incidents even as risk-engineering and siting practices improve.

Cybersecurity is a newer, faster-growing exposure. Battery management systems, inverters and cloud-based energy platforms are internet-connected and remotely updatable, creating entry points malicious actors could use to disrupt charging behaviour or destabilise the grid; and frameworks such as the Australian Energy Sector Cyber Security Framework exist precisely because standalone security measures struggle to cover thousands of diverse, distributed devices.

Two further vulnerabilities are structural. Over-reliance on short-duration, typically four-hour, lithium-ion batteries leaves gaps in genuinely long, multi-day supply droughts, as South Australia's June 2026 wind drought demonstrated. And end-of-life recycling infrastructure remains immature relative to the volume of batteries now being deployed, leaving a future liability policy that has only begun to address it.

MY VIEW ON PRICES

The structural downward pressure on wholesale power prices is expected to continue, even if not in a straight line. BloombergNEF's New Energy Outlook 2026 forecasts solar will become the world's single largest source of electricity generation by 2032, with battery storage the "big mover" behind that shift, and expects Australia's coal exit and storage build-out to keep tracking that global pattern. AEMO's own modelling assumes NEM-wide generation and storage capacity will need to roughly triple by 2050 to meet demand growth from electrification and data centres, implying sustained, multi-decade investment rather than a short-term boom.

On commodities, we expect lithium prices to stay elevated in the near term as inventories rebuild, before moderating from 2027 as a currently oversupplied global market swings back toward balance by 2030. Nickel is expected to firm gradually toward US$17,000/t by late 2027 as Indonesian supply discipline persists, while thermal coal prices - which spiked above $150/t during mid-2026 Middle East disruption and Indonesian export tightening - are expected to ease back toward $110-130 as those disruptions resolve and Asian demand growth slows. The consistent theme is that Australia's dual exposure, as both a major raw-material exporter and an aggressive domestic adopter of the technology those materials build, makes it unusually sensitive to swings in global commodity cycles and domestic wholesale prices at the same time.

CONCLUSION

A year on from the launch of the Cheaper Home Batteries scheme, Australia's storage boom looks less like a passing incentive-driven spike and more like a structural shift in how the grid is built and priced. Batteries now set NEM prices more often than hydro, home storage covers roughly one in 17 households, and AEMO's own planning has been rewritten to assume more storage and less thermal generation than it did twelve months ago. The commodities behind that shift remain volatile and geopolitically exposed, and coal's exit is creating real reliability risk in the short term. How well Australia manages that transition period, more than any single price or policy announcement, will shape its energy system for the next decade.

Connect

info@energizetomorrowus.com

© 2026. All rights reserved.