What is Green, Blue, and Pink Hydrogen? Understanding the Technology, Economics, and Future Outlook

Technological advancements in the energy sector have enabled researchers to explore innovative solutions to drive the transition from conventional power generation sources to cleaner alternatives. With the advent of energy intensive technologies and ever-increasing consumer demand, EIA predicts a 50% increase in global energy consumption by 2050. Efforts to enhance energy efficiency and reduce emissions in this sector have led to the emergence of zero-carbon technologies. Green Hydrogen is one such upcoming technology, especially suited for hard-to-abate sectors like heavy industry, chemicals, and transport, which account for 60% of total energy consumption. Hydrogen finds application in Steel, Ammonia, and Methanol Industries, along with Fuel Cell Electric Vehicles, Electricity Grid Balancing, and Storage. Certain modifications to the sourcing and processes of this technology render innovative alternatives like Blue and Pink Hydrogen. We delve into the technical and economic aspects and explore the future outlook of the Hydrogen Industry.

SUSTAINABLE TECHNOLOGIES

Sumedh Joshi

5/5/20247 min read

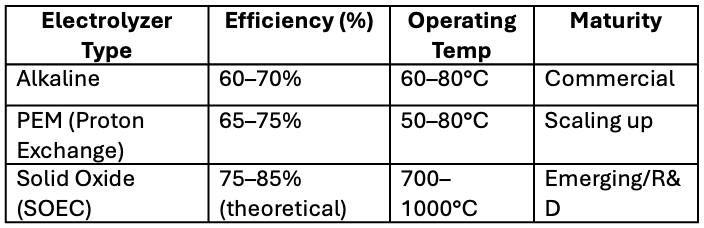

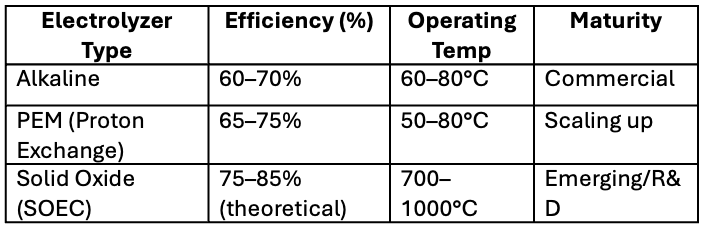

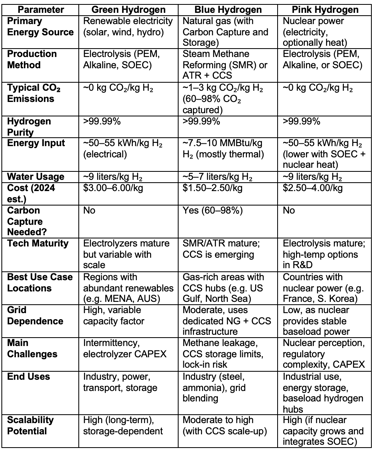

Green hydrogen refers to hydrogen produced via electrolysis of water powered by renewable energy sources such as solar and wind with zero carbon dioxide during production. Current technologies can produce 1 kg of hydrogen with 9 liters of water and 50-55 kWh of electricity. The electrolysis process determines the efficiency of splitting the Oxygen and Hydrogen molecules. There are 3 main electrolyzer types explained below.

Akaline electrolyzers use a liquid aklakine solution (KOH/NaOH)

PEM electrolyzers use a solid polymer membrane, allowing faster response times, and adjusting to fluctuating renewable inputs, especially suited for wind power

SOEC use high temperature steam, potentially increasing efficiency but requiring waste heat integration

Output Metrics -

As of 2025, the electrolyzer CAPEX on an average is $500-1200/kW which is expected to reduce in the coming years. On the other hand, the Levelized Cost of Hydrogen (LCOH) is $6 per kg. According to the EIA, this price is expected to come down to $2/kg, due to electrolyzer advancements, production capacity increases and overall hydrogen consumption.

Challenges of Green Hydrogen include

Intermittent electricity supply reduces capacity factors

High CAPEX/OPEX for large-scale deployment

Storage and transport remain underdeveloped

Water scarcity may limit development in arid regions

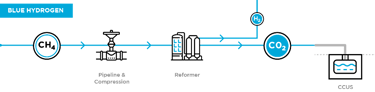

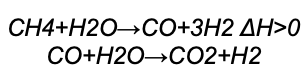

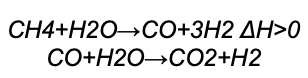

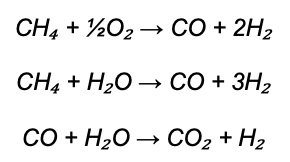

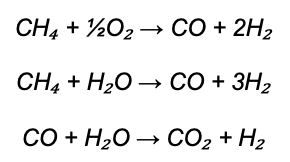

Blue hydrogen is produced by reforming natural gas through Steam Methane Reforming (SMR), Autothermal Reforming (ATR), and Partial Oxidation (POX) combined with Carbon Capture and Storage (CCS) to reduce associated CO₂ emissions.

Steam Methane Reforming -

In SMR, Natural Gas reacts with high temperature steam (700-1000 deg C) in a catalytic reactor. The reaction is exothermic, and CO2 is captured separately.

Typical Hydrogen yield from the Steam Methane Reforming (SMR) is 10 kg/MMBtu of Natural Gas.

Pros: Mature and Cost-Effective

Cons: Lower Carbon Capture Efficiency

Autothermal Reforming (ATR) –

In ATR, Methane reacts with a controlled amount of Oxygen and Steam at 900-1000 deg C. This is an exothermic reaction with a better integration of heat generation and usage. The product of this process is Syngas, rich in H2 and CO2, which is easier to decarbonize with CCS.

Pros: High Carbon Capture Efficiency and Scalability

Cons: Less Mature and Higher OPEX due to Oxygen Supply

Partial Oxidation (POX) -

POX involves the reaction of Methane and Oxygen without Steam. This reaction is exothermic and rapid. A peculiar feature of this process is its superior performance with heavy hydrocarbons or liquid fuels.

Pros: Suitable for low-quality feedstocks

Cons: Low Hydrogen Yield and High CO content

Carbon Capture and Storage (CCS) -

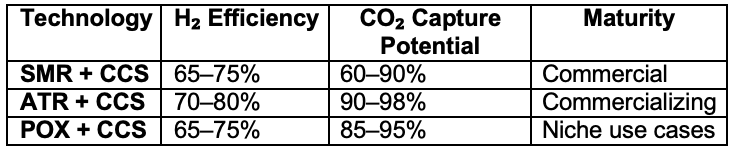

CCS technology for Blue Hydrogen involves Post-combustion and Pre-Combustion capture using amine scrubbing, using solvents like Monoethanolamine (MEA) or pressure swing adsorption. The Carbon Capture efficiencies for Blue Hydrogen Technologies are tabulated below.

With Blue Hydrogen, the Hydrogen production cost, as of 2025, is $2/kg. The CO2 capture intensity achieved with the CCS technologies is 1-3 kg CO2 /kg H2. Total energy input for these processes is 7.5-10 MMBtu per 1 kg of H2. Water use is around 5-7 liters/kg of H2.

Challenges of Blue Hydrogen -

Methane Leakage can erode the climate benefit

CCS scalability poses challenges due to limited geological storage availability

Investment in Blue Hydrogen may delay transition to Green Hydrogen

Pink hydrogen is produced through water electrolysis powered by nuclear energy, offering a near-zero carbon alternative to fossil-fuel-based hydrogen. Unlike green hydrogen, which depends on intermittent renewable sources, pink hydrogen benefits from the consistent baseload power of nuclear plants, allowing electrolyzers to operate at high-capacity factors and improve cost-efficiency. The hydrogen production process using electrolyzers is similar to that of Green Hydrogen.

Output Metrics -

The Hydrogen cost for Pink Hydrogen technologies is $3.5/kg H2. A 1 GW nuclear reactor can produce 180,000 tonnes of H2/year with 50-55 kWh per kg of H2. Water utilization stays the same at 9 liters per kg of H2. Pink Hydrogen works best co-located with nuclear plants to avoid grid transmission losses. Thermochemical cycles, such as the Sulfur-Iodine process and the Hybrid Sulfur process, which are emerging technologies, can convert heat directly into hydrogen with high thermal efficiencies.

Challenges of Pink Hydrogen –

Nuclear Plants and Electrolyzers are capital-heavy

Technology readiness is still in pilot stages

Nuclear power has social and political resistance.

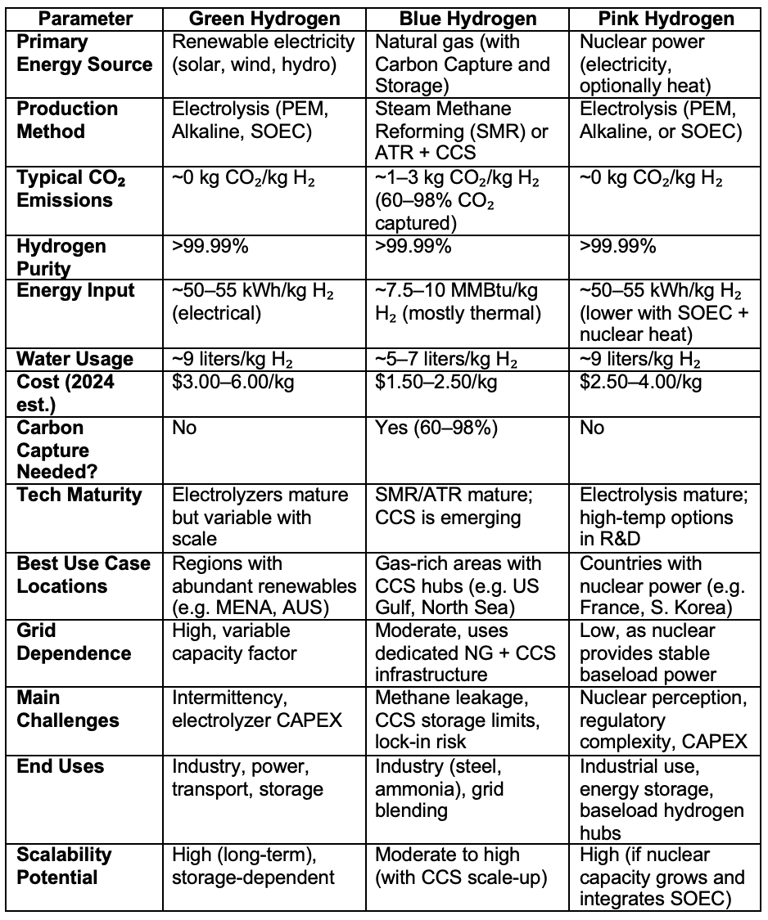

To summarize, the table below differentiates the technologies based on several technical and economic factors.

Economics of Green Hydrogen

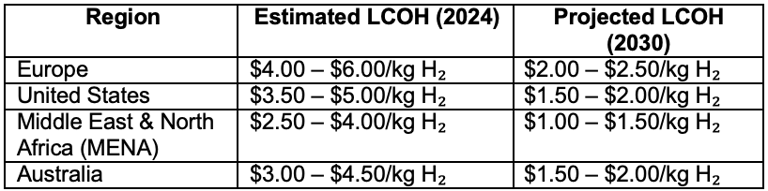

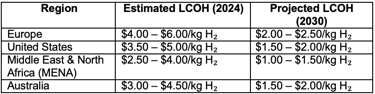

Green hydrogen prices are dominated by electricity costs and utilization rates, with CAPEX falling due to global scaling. Currently, it remains uncompetitive without policy support in most regions but is rapidly approaching commercial viability, especially where cheap renewables and hydrogen subsidies align. The long-term competitiveness hinges on innovations in electrolyzer tech, low-cost solar/wind integration, and flexible demand-side applications. The table shown below gives an idea of LCOH in different global markets.

Green hydrogen economics are highly sensitive to electricity pricing, electrolyzer efficiency, and capacity utilization. A reduction in electricity price by just $10/MWh can lower hydrogen costs by nearly $0.50/kg. Likewise, increasing the electrolyzer efficiency from 60% to 80% can reduce electricity requirements by 10 kWh/kg, yielding significant savings. High Capacity Factors (e.g., 70–80%) enabled by hybrid solar-wind plants or grid balancing will help lower fixed costs for Green Hydrogen facilities. Larger-scale installations also benefit from capital cost dilution, offering better returns on investment as the sector matures.

Despite its sustainability advantages, green hydrogen remains 2–3 times more expensive than gray hydrogen (produced from natural gas) and slightly more costly than blue hydrogen (with CCS) in most regions. This price parity will depend heavily on government policies around the world and flexible demand for efficient storage and a system-wide renewable integration.

Economics of Blue Hydrogen

As of 2025, the levelized cost of Blue Hydrogen typically falls between $1.50 and $3.00 per kilogram, depending on natural gas prices, capture efficiency, and regional CCS infrastructure. This is notably cheaper than green and pink hydrogen in many markets, especially where low-cost gas and storage reservoirs exist (e.g. the U.S. Gulf Coast, Middle East). By 2030, costs may remain stable or slightly decrease if carbon taxes rise, and CCS becomes more scalable.

The biggest cost drivers for blue hydrogen are natural gas feedstock (typically 60–70% of total cost) and the capital and operational expenses of CCS systems. While SMR without capture can cost as low as $1.00/kg, the addition of CCS adds $0.50–1.00/kg, depending on CO₂ concentration, transportation, and storage costs. Blue hydrogen is ideal for industrial applications, including ammonia production, refining, and steelmaking, where continuous large-scale hydrogen supply is critical. Unlike green hydrogen, blue hydrogen benefits from existing natural gas and SMR infrastructure, making it a transitional solution in energy systems where renewable build-out is slow.

Economics of Pink Hydrogen

The LOCH in 2025 is typically in the range of $3.50 to $5.50 per kilogram, depending on the cost of nuclear power and electrolyzer efficiency. This is slightly higher than current blue hydrogen costs and often higher than green hydrogen in regions with cheap renewables. However, in countries with abundant nuclear capacity (e.g. France, Canada, or South Korea), pink hydrogen can be more viable and stable. Future costs could decline to $2.00–$3.00/kg by 2030 as electrolyzer costs drop and the technology is mature. The dominant cost driver for pink hydrogen is nuclear electricity, which can range between $40–$100/MWh, depending on the plant’s age, technology, and region. Pink hydrogen has a very low carbon footprint, comparable to or even better than green hydrogen when accounting for lifecycle emissions. However, environmental concerns surrounding radioactive waste, nuclear safety, and water usage remain politically sensitive. While political resistance to nuclear power persists in some regions, pink hydrogen is increasingly seen as a critical transitional tool, enabling large-scale hydrogen production with minimal emissions and high reliability.

Future Outlook on the Hydrogen Market

Supply Expansion: Clean hydrogen production could triple in 2024 and increase 30-fold by 2030, driven by a surge in electrolyzer shipments and manufacturing overcapacity. - BloombergNEF

Demand Shortfalls: Only 12% of planned clean hydrogen capacity for 2030 has confirmed buyers, with just a tenth of these agreements being binding. – McKinsey & Company

Infrastructure Gaps: Midstream development, including storage and pipelines, is lagging, with initial projects like salt caverns and European pipelines insufficient to meet projected needs.

Investment Bottlenecks: Only 5% of announced capacity for 2030 has reached final investment decisions, indicating hesitancy amidst market uncertainties.

Demand Adjustments: Projected hydrogen demand for 2050 has been reduced by up to 25%, now estimated between 125 and 585 million tons per annum, due to escalating costs and regulatory uncertainties. – McKinsey & Company

Cost Increases: Green hydrogen production costs have risen by 20–40%, attributed to higher capital expenditures and slower technological advancements. – McKinsey & Company

References -

https://www.nationalgrid.com/stories/energy-explained/hydrogen-colour-spectrum

https://www.nexanteca.com/blog/202412/paradigm-shift-hydrogen-production-nuclear-energy

https://www.sciencedirect.com/science/article/pii/S2352484722020625

https://www.engie.com/en/renewables/hydrogen/green-hydrogen-production

https://www.linde.com/clean-energy/our-h2-technology/electrolysis-for-green-hydrogen-production

https://www.energy.gov/eere/fuelcells/hydrogen-production-electrolysis

https://www.iamrenew.com/green-energy/explained-pink-hydrogen-the-future-of-clean-energy/

https://www.woodmac.com/news/opinion/hydrogen-costs-in-2024-what-you-need-to-know/

https://www.utilitydive.com/news/higher-renewable-energy-costs-lazard-lcoe-storage-hydrogen/720177/

https://www.rystadenergy.com/insights/production-of-blue-hydrogen-using-ccs

https://www.utilitydive.com/news/higher-renewable-energy-costs-lazard-lcoe-storage-hydrogen/720177/

https://www.nationalgrid.com/stories/energy-explained/hydrogen-colour-spectrum?

https://www.mckinsey.com/industries/energy-and-materials/our-insights/global-energy-perspective

https://hydrogen-central.com/1h-2024-hydrogen-market-outlook-targets-meet-reality-bloombergnef

Connect

info@energizetomorrowus.com

© 2026. All rights reserved.