The 3T Constraint: How Transformers, Turbines, and Talent Are Throttling the Data Center Boom

In a global survey of data center experts conducted by Turner and Townsend in 2025, 48% of the participants cited “Power” as the top schedule risk. The US interconnection timelines have doubled to 4.5 years from the 2010 levels, partly due to the delayed procurement timelines of “Transformers” needed for grid upgrades. Wood Mackenzie estimates that power transformers and distribution transformers are currently facing a supply deficit of 30% and 6%, respectively, sending the unit prices soaring by 77% compared to 2019 levels. To circumvent this power availability risk, developers are investing in on-site power generation infrastructure, most popularly the natural gas generators, owing to their reliability and shorter build times. IEA estimates that energy developers are planning to build 26 GW of new gas-fired power capacity by 2028, about twice the amount that was planned for 2023-2026. While this opportunity is lucrative for the fast-paced data center industry, gas “Turbine” bottlenecks are a major roadblock. This is partly due to the sheer demand outpacing production capacity, and the gas turbine market being supplied by only 3 major OEMs, who are finding it difficult to ramp up production. Utility-scale gas turbines are being quoted at 48-84 months for new builds, exposing developers to schedule risks. Another major issue surrounds “Talent.” I came across some concerning metrics related to the skilled labor shortage at a Data Center conference I attended last year. The industry needs around 300k-400k skilled construction workers in the next 5 years to meet the growing demand, and the workforce pools are just not enough to fulfill this demand. A study conducted by the Uptime Institute cites that 58% of data center operators struggle to find qualified candidates. Bloomberg also reports that engineering roles that involve advanced physics and complex engineering, such as advanced energy technologies and electrical systems, are facing a shortage, and this gap is estimated to grow to 200k engineering roles by 2030. In this article on bottlenecks in the data center industry, we will explore the dynamics, economics, and the reality of the 3 Ts: Transformers, Turbines, and Talent, and discuss realistic solutions to address/circumvent these bottlenecks.

MOST RECENTENERGY INDUSTRYAI AND ENERGY

Sumedh Joshi

2/28/202610 min read

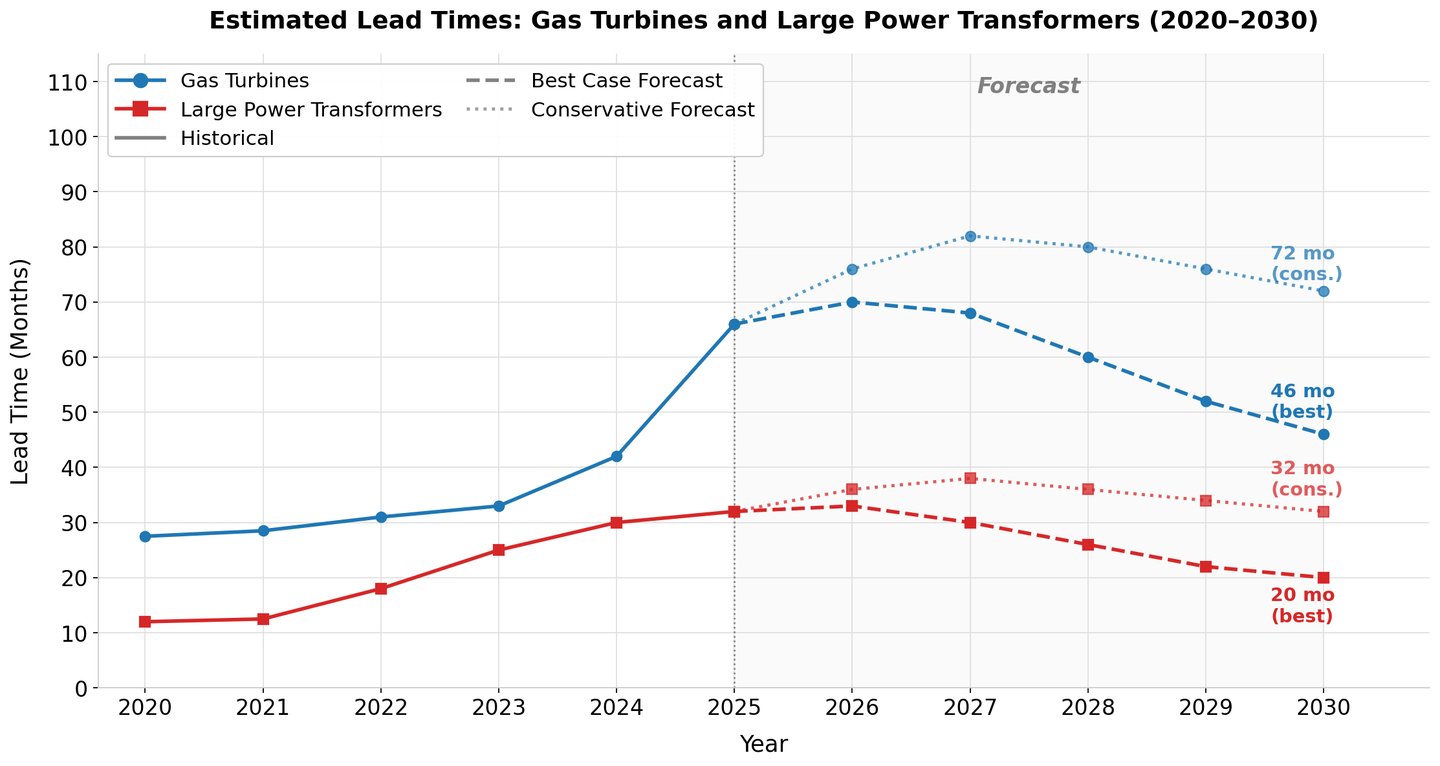

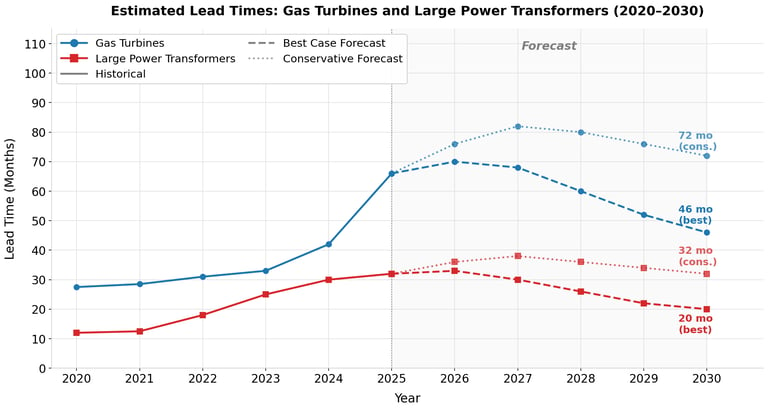

*Details about the above chart are provided in the appendix

Jensen Huang places “Energy Infrastructure” at the foundation of the AI industry layers in his AI analogy. Recent advancements in AI and computing have completely transformed the power equation. Current rack configurations can reach up to 300 KW of IT capacity/rack, enough to power 150 homes. This was utterly unimaginable 10 years ago. The AI boom is real and disruption in the ancillary industries like power and data centers is imminent. This unprecedented growth expectations for the data center industry hinges on a lot of factors, and the most critical ones, Transformers, Turbines, and Talent are discussed below.

1. Transformers:

In 2025, Heathrow Airport faced a massive transformer failure and had to shut down its operations. 1000s of flights were canceled at one of the busiest airports in the world over one piece of equipment in the power infrastructure. That is how critical transformers are, in this modern era, as the IEA calls it, the “age of electricity.” Let us understand the supply-demand dynamics of the transformer market.

The Transformer Demand:

Transformers are an electrical component that increase or decreases electric voltage between two AC power lines. They are critical to the grid such that the US alone has around 80 million small power transformers, one for every 4 residents. For the past few decades, the demand for electricity has stayed flat in the US and Europe, and hence, the grid infrastructure upgradations have been slow. This has totally flipped with the emergence of AI, and the current grid infrastructure is lacking the capability to handle increasing loads. Grid upgradations and expansions generally require a considerable amount of small and large power transformers. A US DOE study found that there are around 80,000 types of different transformers based on their application in the grid. This adds complexity to the supply chain, further increasing lead times. Another report by Utility Drive estimates that 55% of distribution transformers are nearing the end of service life, necessitating upgrades.

The Transformer Supply:

Major supply constraints lie in the sourcing of raw materials. Modern transformers require huge amounts of copper, ceramics, aluminum, and GOES (grain-oriented electrical steel). GOES is a special alloy that is produced at a handful of sites in the US, and a glut of supply comes from Europe, Japan, and China. Copper and aluminum also have constrained supply chain,s and the price volatility can often increase production costs. Additionally, transformers are very complex. Manufacturers often have high standards for reliability, as repairs are time-consuming and very expensive. The figure below shows the transformer delivery times in the US.

It is interesting to note that the lead times on the generation step transformers lie in the 120-170 week range, a massive increase from the 2022 levels. It is possible to increase the production of transformers, but manufacturers are still cautious about expansion, mostly due to the financial lessons from the past boom and busts. In the early 2000s, the industrial growth seemed promising, prompting transformer manufacturers to invest in expanding operations. The demand soon fell with the 2008 financial crisis and left transformer companies with heavy losses on their books. The industry is skeptical of the sustainability of the current rise in transformer demand and is cautious in expanding. However, this is changing with OEMs like GE Vernova, Siemens Energy, and Hitachi Energy expanding production globally.

Realistic Solutions:

A straight solution is to increase production with vertical integration. Companies like ABB have begun localizing their steel-processing and core assembly operations to avoid import delays. This also includes securing long-term contracts with GOES and copper suppliers to lock in prices and holding larger stockpiles of raw materials, largely eliminating price volatility risks. Standardization and modularization of transformers can reduce engineering hours and allow mass production, completely eliminating the delays related to custom designs. GE Vernova, for example, has turned to modular substation designs.

Governments have a role to play in bringing this industry to a safe harbor. The US DOE programs identify GOES production as a critical supply chain risk, creating a healthy environment for domestic GOES production. An extended government effort to provide incentives for domestic transformer manufacturing will go a long way in suppressing supply chain concerns. Simplifying and fast-tracking commissioning and permitting is also a short-term fix to this issue.

Technology also has a role to play here. One of the most promising transformer technologies, with the potential to disrupt the transformer industry, is the Solid-State Transformer. SSTs do not need iron cores and are highly efficient. Current SST technologies are in the research phase, driven by research institutes like NREL and other OEMs. New transformer designs that use amorphous metal alloys instead of GOES can cut down energy consumption significantly. This is being tested in the Japanese and Chinese markets, and successful commercial deployments will reduce the burden on GOES supplies. HTS or high-temperature superconducting transformers are a cutting-edge technology currently in the R&D phase with promising prospects, according to Sumitomo Electric Industries. HTS windings are expected to reduce power losses, shrink transformer size, and reduce copper use. Industry 4.0 components like automation and predictive maintenance is also widely considered to help speed production timelines.

2. Turbines:

Natural Gas contributes 40% to the energy generation in the US, and 22% globally. It is widely viewed as a transition fuel between coal and clean energy, with emerging markets driving 75% of growth. Governments in the emerging economies view natural gas as a low-carbon alternative to coal due to its abundant supply and well-established technology prospects. On top of this, the AI boom has unlocked new opportunities for gas-fired power plants as a growing choice for on-site power. Gas power plants offer reliable base-load power and have very short start-up times, making them ideal for data center power.

The Turbine Demand:

As mentioned earlier, energy developers are planning to build more than 26 GW of new gas-fired power plants by 2028 to keep up with the 25% increase in the power demand in the US by 2030. This sudden demand increase for gas-fired plants is not local. According to Goldman Sachs, Europe needs $500 B investment in gas-fired plants and battery storage until 2030 to counter the increasing power demand that had flatlined for the past 15 years. China is poised to sanction the construction of 70 GW of gas plant capacity by 2030.

Gas turbines are an integral component of these power plants. They are rotary devices with rotor and stator blades that capture usable energy from the combustion of natural gas. A utility-scale gas turbine often weighs 500 tons with a complex and high-precision assembly. This industry is dominated by 3 major players, GE Vernova (25% market share), Siemens Energy (24%), and Mitsubishi Heavy Industries (22%). The turbine industry is a perfect example of an oligopoly, and high entry barriers render new entrants unable to disrupt. With a sudden turbine demand spike related to AI, manufacturers are receiving a huge number of orders. Data center developers and utilities are locking up supply with these manufacturers like never before. For example, NRG Energy, a Houston-based utility provider, has signed a deal with GE Vernova to develop 5.4 GW of gas-fired power plants between 2029 and 2032. GE Vernova already has turbines booked as far out as 2030 and Mitsubishi Heavy Industries until 2028, and lead times have grown to 48-84 months for large gas turbines. This extreme demand has pushed gas power plant prices from $800/kW in 2021 to $2500/kW in 2026, also sending the turbine industry stocks soaring. Bloomberg reports that this bottleneck exposes $400 B worth of gas-fired power plant projects to delays and cancellation risks.

The Turbine Supply:

The supply issue has surfaced due to two important factors. The restrictive nature of market entry and the unwillingness of these manufacturers to expand production. Turbines are hard to manufacture and require huge amounts of investment and research. Turbine blades cannot be mass-produced due to complex manufacturing processes with Single-Crystal (SX) and high-temperature nickel-based alloy. The fabrication houses that supply these forgings and castings have huge backlogs. Turbines are also susceptible to supply chain issues for component sourcing. Turbine combustor and fuel nozzles have a lead time of 5-9 months, which can skew the turbine delivery schedule. Additionally, nickel alloys, a critical material for turbine production is known for their choppy price characteristics and can inflate delivery budgets.

Similar to the transformer industry, the turbine industry has fallen prey to past boom and bust episodes, forcing companies to follow a cautious approach. While manufacturers have been investing in expanding production, like GE Vernova investing $300 M to build plants in South Carolina and New York, and Mitsubishi Heavy Industries boosting production capacity by 30%, the demand is steeply outpacing supply.

Realistic Solution:

Governments need to step in and treat turbine blades as critical national infrastructure. Other than that, to address the forging and casting bottlenecks, governments should offer capital subsidies to manufacturing facilities. Turbine manufacturers also need to diversify their suppliers and build local facilities to address local needs. Vertical integration is another solution to bring end-to-end manufacturing capabilities under one single umbrella, thereby simplifying the procurement process.

Technology advancement, undeniably, has a big role to play here. Additive manufacturing has been around for some time and is reliably used to manufacture intricate and high-quality parts. Turbine components like fuel nozzles, cooling-channel components, and small turbine blades can be manufactured using additive manufacturing. GE Vernova has been using additive manufacturing for some of its components and is able to move away from casting and forging. Material advancements like new superalloys that eliminate supply burdens on conventional materials will prove beneficial. Modularization of turbines can also help streamline manufacturing and condense delivery timelines. Turbine life extension programs are another way to extend the operational life of existing turbines, thereby reducing demand for new orders. Manufacturers have begun investing in these programs to meet high demands, with GE Vernova and MD&A being at the forefront.

3. Talent

A WEF report shows that over half of data center operators struggle to attract and retain qualified staff, creating a huge talent gap. This could cost the data center industry over $449.7 B globally. The root cause of this problem comes from workforce retirement. Over 33% of the technical workforce in the data center industry is nearing the age of retirement. New hires only make up about 16% of the workforce, forcing a talent gap that is expected to grow every year. The biggest gap is in junior and mid-level operations roles, followed by mechanical and electrical positions. On the construction side, over 400 under-development data centers face backlogs due to staff shortage.

The Talent Gap:

AI is a fast-paced industry, necessitating data center operators to constantly keep pace with hardware development, which can create a talent gap. This gap widens if the workforce is not trained appropriately to deal with new technologies, construction methods, and cybersecurity. This is exacerbated by a misalignment between educational curriculum and data center job qualifications, with only 15% of the total applicants satisfying the minimum job requirements.

This talent gap is the widest in the electricity infrastructure and HVAC, making electricians and plumbers a hot commodity. Data centers compete with other industries like manufacturing plants and housing for electricians and plumbers, squeezing the talent pool even further. Data center jobs pay well above what an electrician or a plumber would make on a housing development project, creating cross-industry ramifications. This also has wider consequences as workers are now moving to the frontier states like Arizona and Texas, leaving other states with smaller labor pools. Skilled trade is estimated to require 400k workers in the next 5 years to support data center industry growth. The skilled trade talent pool is not big enough to undertake this task.

Mainstream engineering pipelines are also facing a widening workforce shortage. It is estimated that around 17,500 electrical and electronics engineer positions are seeking candidates on an urgent basis in the US. The shortage translates to higher salaries for on-site workers, which is often more than instructor position roles, further exacerbating the talent gap by incentivizing workers to select on-site roles over training roles. Advancements in liquid cooling have boosted demand for Mechanical engineers who are offered an incentive for higher pay in the data center industry, transition from other industries, creating a cross-domain workforce shortage. The civil engineering domain also faces a talent shortage, delaying commissioning and other important construction milestones.

This shortage of Mechanical and Electrical engineers is an important reason for turbine and transformer bottlenecks. Manufacturers are finding it difficult to hire enough engineers, often delaying expansion plans and R&D initiatives. This workforce shortage could be linked to an incentivization gap between tech jobs and core engineering jobs. Since the 2000s, universities have seen a steady rise in students opting for software engineering as their major, often due to better career prospects. This has created a shortage of engineers in core engineering fields, but this gap is expected to shorten as the software industry grows more saturated. AI might replace software engineers with coding-related jobs, which is expected to push more and more engineers towards the conventional fields like Mechanical and Electrical Engineering.

Realistic Solution:

Academia and industry partnerships are necessary to bridge the talent gap with continuous skill development, increase upskilling budgets, and create accessible training pathways. Microsoft and Google have invested in skilling programs across the US, blending classroom learning with hands-on experience. Certification and apprenticeships are crucial for fast-track upskilling. Certifications like CDCP (Certified Data Center Professional), PMP, and vendor-specific certifications ensure that the workforce is qualified to undertake work tasks. Cross-industry migration to some extent is necessary as the required workforce already exists in other fields. Expanding the talent pipeline to accept candidates from other technology fields or career changers and veterans will help bridge the gap. Automation will significantly reduce the burden on the talent pool by automating tasks that are sequenced and require precision and can be undertaken by machines. Many developers are moving towards modularization of data centers in an attempt to reduce labor requirements at the construction site. Individual modules like power, IT racks, and cooling can be manufactured off-site and then shipped to be assembled on the construction site. This eliminates the need for additional construction workers, plumbers, electricians, and operations personnel.

Conclusion:

AI has been a transforming force in the current times. The pace of this growth has created enormous demand for critical power components like transformers and turbines, where talent remains a massive bottleneck. Markets often correct themselves to achieve equilibrium, and with the amount of incentives AI brings along with it, manufacturers will eventually expand production to match the demand. This is also true about the talent pool. An influx of capital into the data center industry will eventually attract talent from trade schools, universities, and cross-technology talent pools.

*The conservative and the best-case scenarios for lead times on transformers and turbines based on market reports from Wood McKinzie, Bloomberg, and OEM forecast reports. The lead times are expected to ease in both scenarios, with the best-case scenario showing a significant decrease in the lead times by 2030. The conservative scenario is a possibility if the bottlenecks and their actors persist. Nevertheless, development in alternative power technologies like fuel cells, renewables, batteries, and nuclear will ameliorate the impact of these 3T bottlenecks.

Connect

info@energizetomorrowus.com

© 2026. All rights reserved.